Introduction

According to Fortune Business Insights, the global cloud computing (CC) SaaS market is projected to have a CAGR of 18.4% between now and 2032 which should bode well for CC companies. This article highlights the 7 largest pure-play cloud computing SaaS software companies. (Before proceeding listen to the MunAiMarkets theme song and get in the mood to join the rich man’s world!)

What is Cloud Computing?

Cloud computing (CC) is the technique of processing, storing, and managing data on a network of remote computers hosted on the internet by cloud service providers rather than on a personal computer or local server using only as much compute power and storage as needed to meet demand. This theoretically allows for cheaper and faster computing because it eliminates the need to purchase, install, and maintain servers.

What is SaaS?

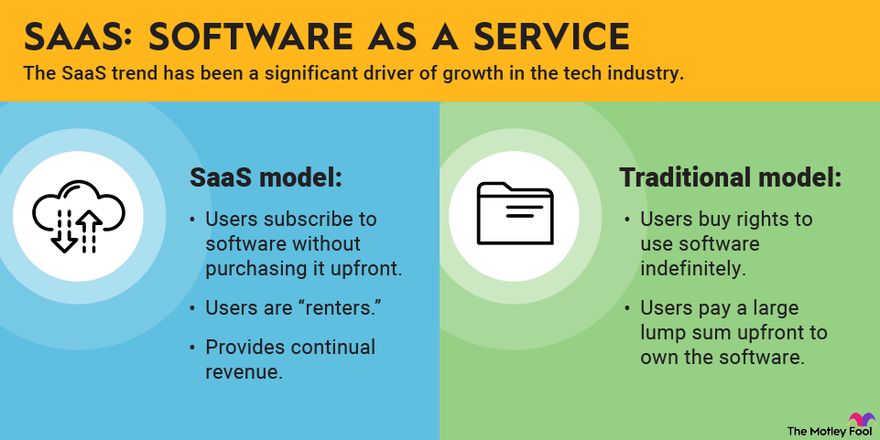

SaaS, also known as cloud application services, makes software available to users over the internet, usually for a monthly subscription fee. They are typically ready-to-use and are run from a users’ web browser which allow businesses to skip any additional downloads or application installations. SaaS accounts for 38.5% of cloud computing revenue. (Source) For more insightful information you are encouraged to read Cloud Computing 101.

Image source: The Motley Fool

What’s the current state of the SaaS industry?

SaaS transformed the global enterprise software market growing at double the rate of the overall market between between 2100 and 2018 but it has slowed since then with the reduction in IT spending as interest rose leading to cash flow issues and the recent unprecedented growth of gen AI has disrupted the software industry even faster and more thoroughly than SaaS.

What Impact Will Gen AI Have On the Software Space and, By Extension, the SaaS Market?

Gen AI allows software leaders to reexamine and address customer needs in a totally new way, as well as to explore adjacencies they hadn’t thought of before and McKinsey research indicates that gen AI will trigger software customers to switch their vendors more frequently – by 5-10 percentage points -as they race to keep up with the latest innovations. As such, SaaS companies will do well to prepare for this shift by:

- working to both keep up with software application development;

- protecting existing client relationships by reexamining and addressing customer needs in a totally new way;

- exploring adjacencies they hadn’t thought of before;

- considering how they price and package their products;

- evaluating how they gather and use their proprietary data; and

- revamping product strategy and their road map for the gen AI era.

How can new SaaS business building help organizations drive growth?

Growth is a constant goal—and challenge—for most companies. We’ve found that many companies expect to get as much as 50 percent of their revenue from new businesses and products by 2026. SaaS can help by allowing companies access to all the software services they need without having to create the software themselves but most organizations are not on a path that will get them there. In fact, only 6% of global software revenues are earned by non=tech companies.

What Is the PEG Ratio?

Given that growth is a key component of a stock’s expected return, the PEG ratio provides a simple way for investors to see how cheap a stock is relative to its growth rate and compare it to its competitors.

The PEG ratio (price/earnings-to-growth ratio) builds upon the price-to-earnings (P/E) ratio by factoring in expected earnings growth. It takes into account not just the current earnings but also the company’s growth prospects. It is a quick calculation used to determine if a stock is trading at, above, or below fair value.

- A PEG ratio below 1.0 suggests that the stock price is undervalued relative to its expected future earnings growth. In other words, the market may not fully account for the company’s growth potential.

- Conversely, PEG ratios above 1.0 indicate that the stock price might be overvalued, as it isn’t necessarily supported by growth forecasts.

- Look for stocks with a PEG ratio below the industry median.

- The PEG ratio should be used along with the balance sheet, debt burden, and cash flow, or other valuation metrics that use the income statement. It’s also important to understand things like a company’s competitive advantage, its addressable market, and its long-term growth prospects.

- It’s a convenient rule of thumb but remember that the PEG ratio can vary based on earnings growth forecasts and the time frame being considered.

What is the Price-to-Sales Ratio?

The price-to-sales (P/S) ratio, which equals a company’s market capitalization divided by its annual revenue, is often used as a valuation metric for SaaS companies in place of the P/E ratio. A higher P/S ratio denotes optimism among investors that attractive revenue growth will continue and that the revenue will eventually generate profits.

The MunAiMarkets Pure-Play Cloud Computing SaaS Stocks Portfolio

Below is a list of the 7 largest pure-play cloud SaaS software computing companies presented in descending order of their performances MTD, and in 2024, their forward price-to-earnings, price/earnings-to-growth ratios, their forward price-to-sales ratios and the reasons behind their price changes:

- Cloudflare (NET): UP 8.8% MTD; UP 29.3% in 2024

- Forward Price-to-Earnings Ratio: 149

- Price/Earnings-to-Growth Ratio: 2.9

- Forward Price-to-Sales Ratio: 20.3

- Reasons for Price Change:

- Analyst Upgrades: Citigroup upgraded Cloudflare’s rating from “Neutral” to “Buy” and raised the price target from $95 to $145 boosting investor confidence.

- Strong Financial Performance: Cloudflare reported strong financial results, with revenue growth of 28% year-over-year in Q3 2024 and this growth has been a positive signal to investors.

- Market Sentiment: The recent Consumer Price Index (CPI) data showed lower-than-expected inflation, which may lead to more rate cuts by the Federal Reserve which is beneficial for growth stocks like Cloudflare.

- Positive Market Trends: The S&P 500 and Nasdaq Composite indices were also up, contributing to the overall positive market sentiment.

- MongoDB (MDB): UP 8.7% MTD; DOWN 43.2% in 2024

- Forward Price-to-Earnings (P/E) Ratio: 82

- Price/Earnings-to-Growth (PEG) Ratio: 4.7

- Forward Price-to-Sales Ratio (PSR): 8.5

- Reasons for Price Change:

- Analyst Upgrades: Multiple analysts upgraded their ratings for MongoDB: Guggenheim raised its rating from “Neutral” to “Buy” with a price target of $300, and Cantor Fitzgerald initiated a “Strong Buy” rating with a price target of $344.

- Strong Financial Performance: MongoDB reported impressive Q3 2024 earnings, with revenue growth of 22.3% year-over-year, surpassing consensus estimates.

- Positive Market Sentiment: The overall positive sentiment in the tech sector and the broader market also contributed to the stock’s rise.

- Atlassian (TEAM): UP 3.7% MTD; UP 2.3% in 2024

- Forward Price-to-Earnings Ratio: 73

- Price/Earnings-to-Growth Ratio: 2.9

- Forward Price-to-Sales Ratio: 12.1

- Reasons for Price Change:

- Analyst Upgrades: Multiple analysts upgraded their ratings for TEAM. For instance, Keith Weiss from Morgan Stanley maintained a “Buy” rating and raised the price target from $259 to $315.

- Strong Financial Performance: Atlassian reported impressive fiscal second-quarter results, showcasing a 21% year-over-year revenue increase, which surpassed consensus forecasts by 4%. Billings also surged by 25% year-over-year.

- Positive Market Sentiment: The overall positive sentiment in the tech sector and the broader market contributed to the stock’s rise.

- HubSpot (HUBS): UP 1.1% MTD; UP 20.0% in 2024

- Forward Price-to-Earnings Ratio: 80

- Price/Earnings-to-Growth Ratio: 3.1

- Forward Price-to-Sales Ratio: 14.3

- Reasons for Price Change:

- Analyst Upgrades: Multiple analysts upgraded their ratings for HUBS. For instance, Keith Weiss from Morgan Stanley maintained a “Buy” rating and raised the price target from $747 to $835.

- Strong Financial Performance: HubSpot reported impressive fiscal second-quarter results, showcasing a 21% year-over-year revenue increase, which surpassed consensus forecasts.

- Positive Market Sentiment: The overall positive sentiment in the tech sector and the broader market contributed to the stock’s rise.

- ServiceNow (NOW): UP 1.1% MTD; UP 49.9% in 2024

- Forward Price-to-Earnings Ratio: 69

- Price/Earnings-to-Growth Ratio: 2.1

- Forward Price-to-Sales Ratio: 17.4

- Reasons for Price Change:

- Analyst Upgrades: Multiple analysts upgraded their ratings for NOW: Guggenheim raised its rating from “Neutral” to “Buy” with a price target of $300, and Cantor Fitzgerald initiated a “Strong Buy” rating with a price target of $344.

- Strong Financial Performance: ServiceNow reported impressive Q3 2024 earnings, with revenue growth of 22.3% year-over-year, surpassing consensus estimates.

- Positive Market Sentiment: The overall positive sentiment in the tech sector and the broader market also contributed to the stock’s rise.

- Datadog (DDOG): DOWN 3.1% MTD; UP 17.7% in 2024

- Forward Price-to-Earnings Ratio: 74

- Price/Earnings-to-Growth Ratio: 3.6

- Forward Price-to-Sales Ratio: 15.0

- Reasons for Price Change:

- Analyst Downgrades: Morgan Stanley downgraded DDOG from “Overweight” to “Equal Weight,” citing concerns about the company’s fiscal 2025 financial results potentially falling below analysts’ average estimates.

- Revenue Concerns: Analysts noted that only 68% of Datadog’s forward revenue is under contract, which is below the firm’s initial guidance of 72%. This raised concerns about the company’s ability to meet revenue targets.

- Earnings Estimates Cut: Capital One Financial lowered their Q1 2025 earnings estimates for Datadog, which added to the negative sentiment.

- Market Reaction: The stock market reacted to these concerns, leading to a 3% drop in DDOG’s stock price following the downgrade.

- Workday (WDAY): DOWN 3.3% MTD; Down 6.5% in 2024

- Forward Price-to-Earnings Ratio: 32

- Price/Earnings-to-Growth Ratio: 1.1

- Forward Price-to-Sales Ratio: 7.0

- Reasons for Price Change:

- Disappointing Earnings Report: Workday’s Q3 2024 earnings report fell short of analysts’ expectations, which negatively impacted investor sentiment.

- Revenue Guidance: The company provided weaker-than-expected revenue guidance for the upcoming quarters, raising concerns about future growth.

- Market Reaction: The stock market reacted to the earnings report and guidance, leading to a decline in WDAY’s stock price.

- Competitive Pressure: Increased competition in the enterprise software market also contributed to the stock’s decline.

Summary

The above 7 pure-play cloud SaaS computing stocks model portfolio is UP 1.6% MTD and went UP 4.9% in 2024.

Conclusion

According to Fortune Business Insights, the global cloud computing SaaS market is projected to have a CAGR of 18.4% between now and 2032 which should bode well for CC companies.

Like our new site? Here are 10 ways to get involved:

- Listen to the MunAiMarkets theme song and join the rich man’s world!

- Follow MunAiMarkets on Facebook and never miss an article.

- Share this article on LinkedIn, X and/or Pinterest.

- Watch our latest video posts on youtube.

- Comment on the articles and ask any questions you have.

- Submit an article for posting consideration.

- Become the site’s primary contributor and a full partner.

- Advertise on the MunAiMarkets banner for a token $10/mo. in 2025.

- Sponsor one of the site categories or an individual article for a modest fee.

- Support our efforts with a modest financial contribution.