An Introduction

Lance Roberts points out in his latest article that, “with slowing economic growth, fiscal policy uncertainties, global challenges, overconfident sentiment, and ambitious earnings expectations, investing in 2025 will require a blend of optimism and caution. have plenty of reasons to approach the markets carefully. Taking advantage of bullish advances while they last is essential. Just don’t become overly complacent, believing, “This time is different.” It likely isn’t. A good portfolio management strategy will ensure exposure decreases and cash levels rise when the selling begins.” Below are 5 reasons why Roberts says – in edited and abridged excerpts – that “a more cautious approach to investing might be warranted in 2025.”

1. Valuations & Economic Growth Rates

The S&P 500’s price-to-earnings (P/E) ratio currently sits well above its historical average, signaling investor exuberance. While valuations are a terrible market timing indicator and should never be used as such, they do tell us much about investor sentiment….and current valuations suggest that stocks are priced for perfection as investors bid up asset prices ahead of what a declining economic growth rate can deliver. This leaves little room for error. In other words, investors are essentially betting on corporations’ flawless execution in a year when macroeconomic uncertainties loom large.

…Signs of a slowdown are emerging as we enter 2025. The Federal Reserve’s recent interest rate cuts may have provided short-term relief, but their effectiveness in sustaining long-term growth remains uncertain. Consumer spending, a critical driver of the economy, has shown signs of fatigue as households face diminishing savings and rising debt levels. If economic growth slows in 2025, it could dampen corporate revenue, reduce investment activity, and impact stock prices...The risk of weaker growth looms large, potentially catching overconfident investors off guard.

2. Fiscal Policy & Global Economic Growth Rates

…Over the past two years, ongoing fiscal policy from the Inflation Reduction and CHIPs Acts and ongoing increases in federal spending through “continuing resolutions” have supported economic growth. However, in 2025, reductions in fiscal policy may become a headwind as previous spending bills are exhausted without new ones to take their place. Furthermore, reductions in government spending by the incoming Administration via the Department of Government Efficiency could provide an additional drag on economic growth.

…Additionally, the U.S. is not the only player in the global economy. Growth rates in key regions like Europe and China are slowing, adding another layer of uncertainty… as the relationship between the U.S. economy and the European Union, OECD nations, and the rest of the world is incredibly high… and while very short-term divergences occur but, barring a change to the world trade order or another round of massive US stimulus, it’s improbable that recent divergences will last.

While significant Federal deficit spending has boosted economic growth and offset higher borrowing costs and inflation, there are indications that support is slowing. Furthermore, the U.S. is not an “island of economic prosperity” but a global trade partner. As such, slowing global growth could dampen demand for U.S. exports, further pressuring corporate earnings, which…remain exceptionally deviated from long-term growth trends and economic activity…and weaker international growth could derail the optimistic narrative investors are currently embracing.

3. The Technical Backdrop

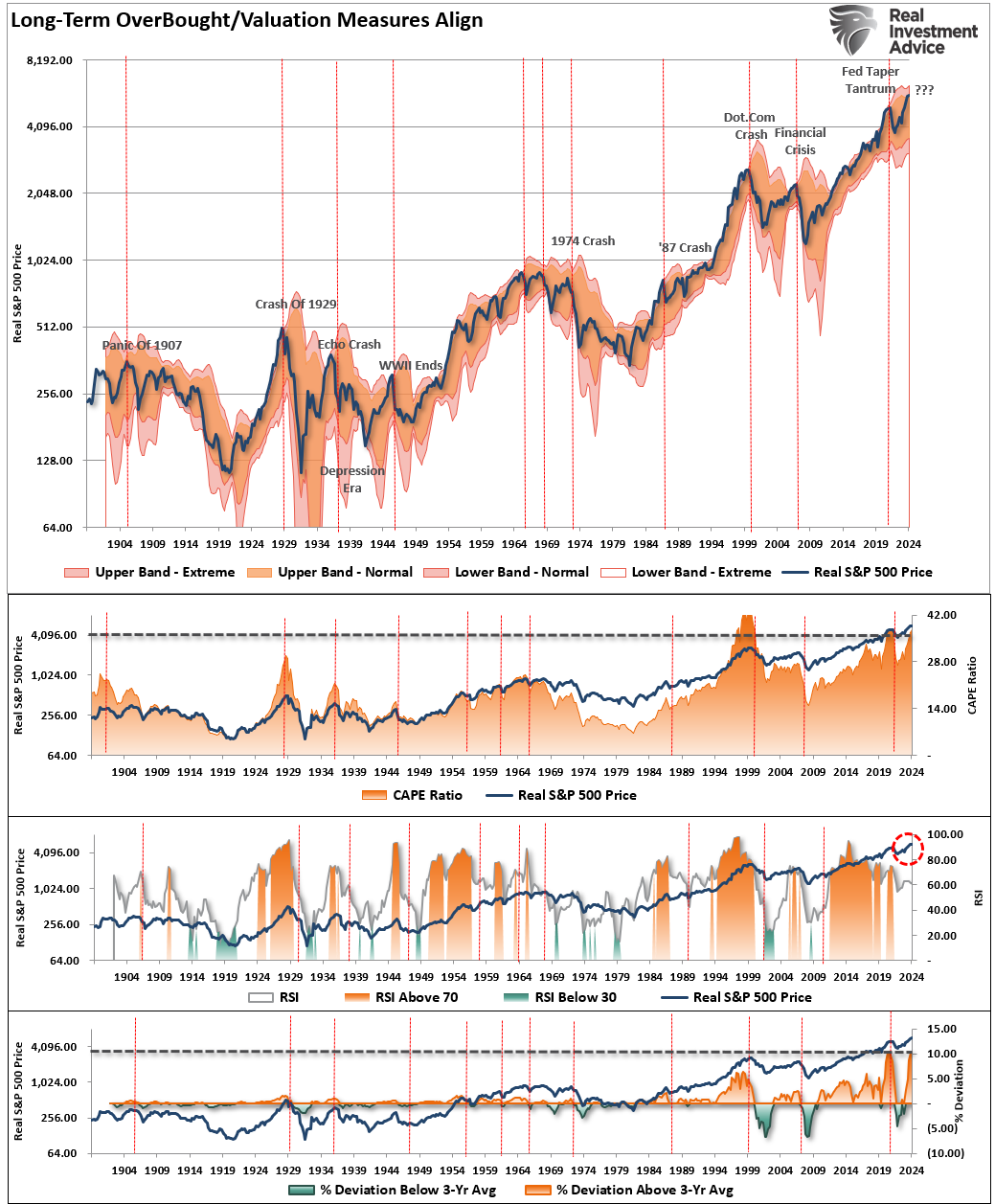

…A market melting-up is exciting while it lasts. During melt-ups, investors rationalize why ‘this time is different.’ They start taking on excess leverage to try and capitalize on the rapid advance in prices, and fundamentals take a back seat to price momentum. Market melt-ups are all about ‘psychology.’ Historically, whatever has been the catalyst to spark the disregard of risk is readily witnessed in the corresponding surge in price and valuations. The chart below shows the long-term deviations in relative strength, deviations, and valuations. The previous ‘melt-up’ periods should be easy to spot when compared with the current advance.

It is worth noting in the chart that:

- prices are again deviating from the long-term mean,

- valuations are extended,

- relative strength is declining.

Furthermore,

- investors are taking on increasing speculative risk and leverage, just as they were in 2021 and

- expectations for corporate earnings, the lifeblood of market performance, appear overly ambitious with analysts projecting a nearly 20% increase in earnings for the year, a figure well above historical trends. These projections, however, may not align with economic realities, particularly if consumer demand softens, the global economy slows further, or cost pressures persist.

In 2024, actual earnings growth fell short of forecasts, with much of the market’s performance driven by valuation expansion rather than fundamental earnings growth. If this pattern continues, the risk of a correction increases and such a risk is something to seriously consider heading into the new year.

Conclusion

…While 2025 presents its share of challenges, none of this means the next “bear market” is lurking. The solution is not to abandon the market altogether. Instead, investors need guidelines to participate in the market advance and to take practical steps to navigate these uncertainties…

- Tighten up stop-loss levels to current support levels for each position. (Provides identifiable exit points when the market reverses.)

- Hedge portfolios against significant market declines. (Non-correlated assets, short-market positions, index put options)

- Take profits in positions that have been big winners. (Rebalancing overbought or extended positions to capture gains but continuing to participate in the advance).

- Sell laggards and losers. (If something isn’t working in a market melt-up, it most likely won’t work during a broad decline. It is better to eliminate the risk early.)

- Raise cash and rebalance portfolios to target weightings. (Rebalancing risk regularly keeps hidden risks somewhat mitigated.)

Notice, nothing in there says, “Sell everything and go to cash.” Taking advantage of bullish advances while they last is essential. Just don’t become overly complacent, believing, “This time is different.” It likely isn’t. Just remember, as Larry David might say, “You don’t have to be a genius—just don’t be a schmuck.”

Like our new site? Here are 10 ways to get involved:

- Listen to the MunAiMarkets theme song and join the rich man’s world!

- Follow MunAiMarkets on Facebook and never miss an article.

- Share this article on LinkedIn, X and/or Pinterest.

- Watch our latest video posts on youtube.

- Comment on our articles and ask any questions you have.

- Submit an article for posting consideration.

- Become the site’s primary contributor and a full partner.

- Advertise on the MunAiMarkets side panel for a token $10/mo. in 2025.

- Sponsor one of the site categories or an individual article for a modest fee.

- Support our efforts with a financial contribution.